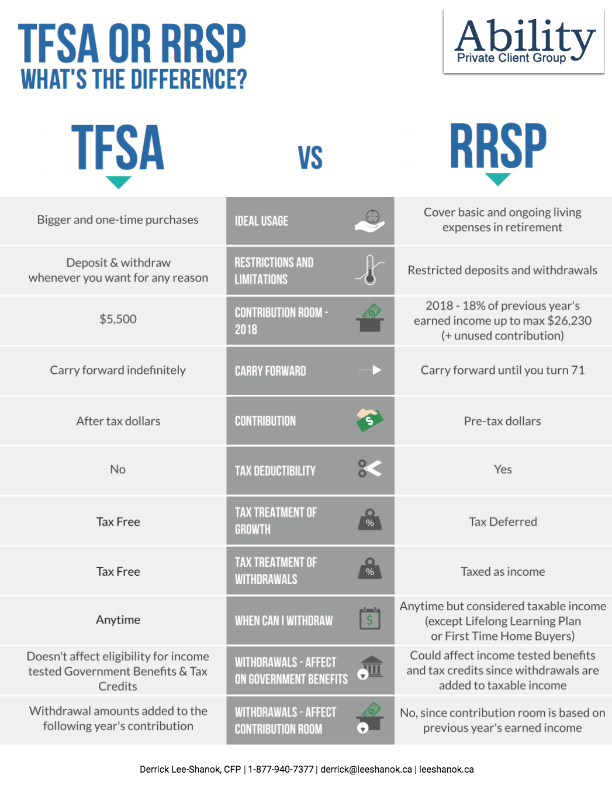

If you are seeking ways to save in the most tax-efficient manner available, TFSAs and RRSPs can both be effective options for you to achieve your savings goals more quickly. However, each plan does have distinct differences and advantages / disadvantages. Let’s take a look at their key features:

In summary, your individual circumstances will dictate which plan is the most appropriate for you, depending on your tax position and withdrawal intentions. The primary difference between both plans is the timing of the taxes payable i.e. if you want to defer the payment of your taxes, particularly if your marginal tax rate will be lower in retirement, an RRSP may be more beneficial for you. Alternatively, if your marginal tax rate will be higher when you plan to make withdrawals, a TFSA may suit you better.

Mutual funds, approved exempt market products and/or exchange traded funds are offered through Investia Financial Services Inc.

Insurance products are offered through PPI Management Inc., a national licensed insurance marketing organization that support independent advisors with their business, and through multiple insurance companies.